Inside Numerai's 13F: What The Hedge Fund Actually Holds

Numerai's year-end 2025 13F reports $830M across 608 US equity positions, with the largest holding just 1.06% of the book — a systematic fingerprint.

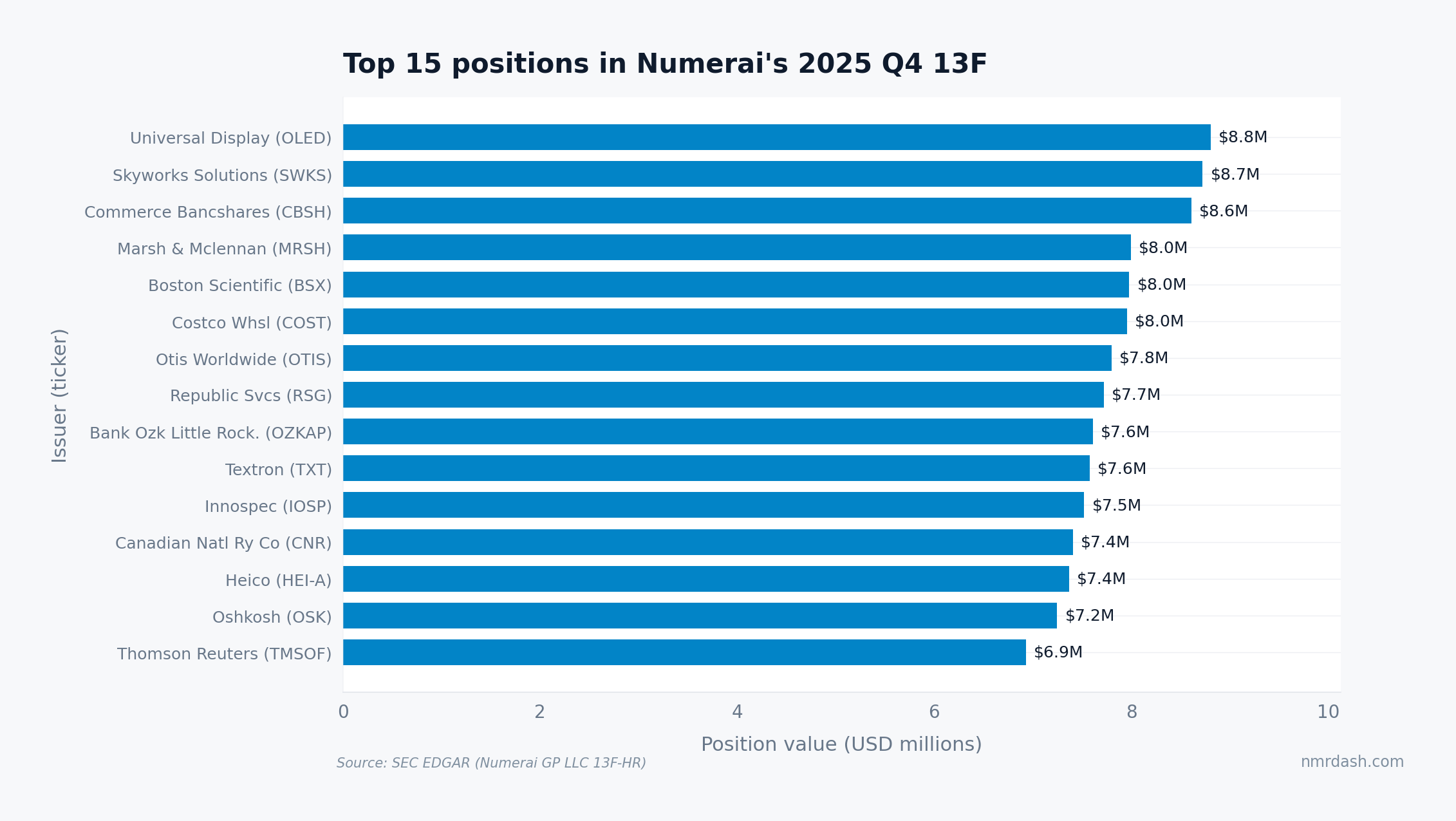

Numerai's year-end 2025 13F filing reports $830M of US equity positions across 608 line items, and the single largest holding, Universal Display Corp at $8.8M, is only 1.06% of the book. That is consistent with a systematic quant book, not a high-conviction stock picker. The holdings dashboard tracks every quarter live; this post pulls apart what is actually inside.

A companion piece, Numerai SEC Filings: 13F and Form ADV Footprint, covers the macro view: one filer, 13 quarters, headline AUM. This article goes inside that filer to read the portfolio itself.

The names at the top of the book

Numerai's largest 13F position at year-end 2025 was Universal Display Corp (OLED) at $8.8M, followed by Skyworks Solutions ($8.7M) and Commerce Bancshares ($8.6M). The top 15 positions together account for $117M, which is 14% of the $830M book.

The shape of the bars matters more than the names. There is no anchor position. The top 15 holdings span $8.8M down to $6.9M, a 28% spread. A concentrated long-only fund usually puts 5% to 10% of NAV in its top name; here every position is a small bet pulled from a long, flat list. Voting authority is sole on every share: voting_shared and voting_none are both zero across all 608 holdings, consistent with a single managed account rather than sub-advised mandates.

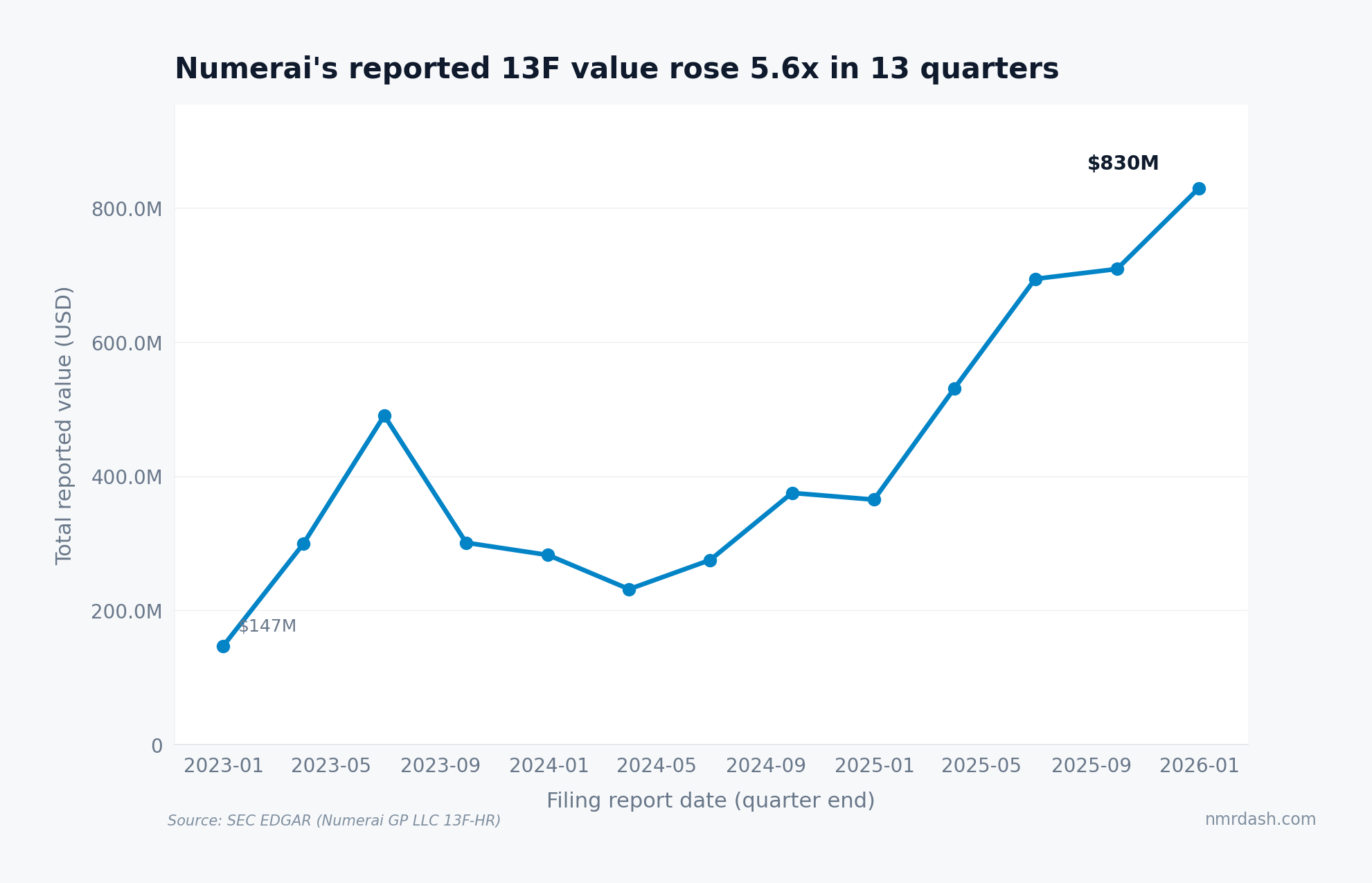

Reported value scaled 5.6x in three years

Total reported 13F value rose from $147M at year-end 2022 to $830M at year-end 2025, a 5.6x increase across 13 quarters. The path was not monotonic. Q2 2023 spiked to $490M before settling back near $300M for the rest of that year, dipped to about $230M in early 2024, then climbed steadily through 2025.

Two forces can explain the rise. The fund itself has grown; Numerai's Form ADV reports cross $1B in adviser AUM during the same window. Equity market beta also inflated reported values, since 13F values are pinned to quarter-end prices. The Q2 2023 spike could reflect a temporary position ramp, portfolio transition, or reporting-date effect; the 13F alone cannot distinguish those.

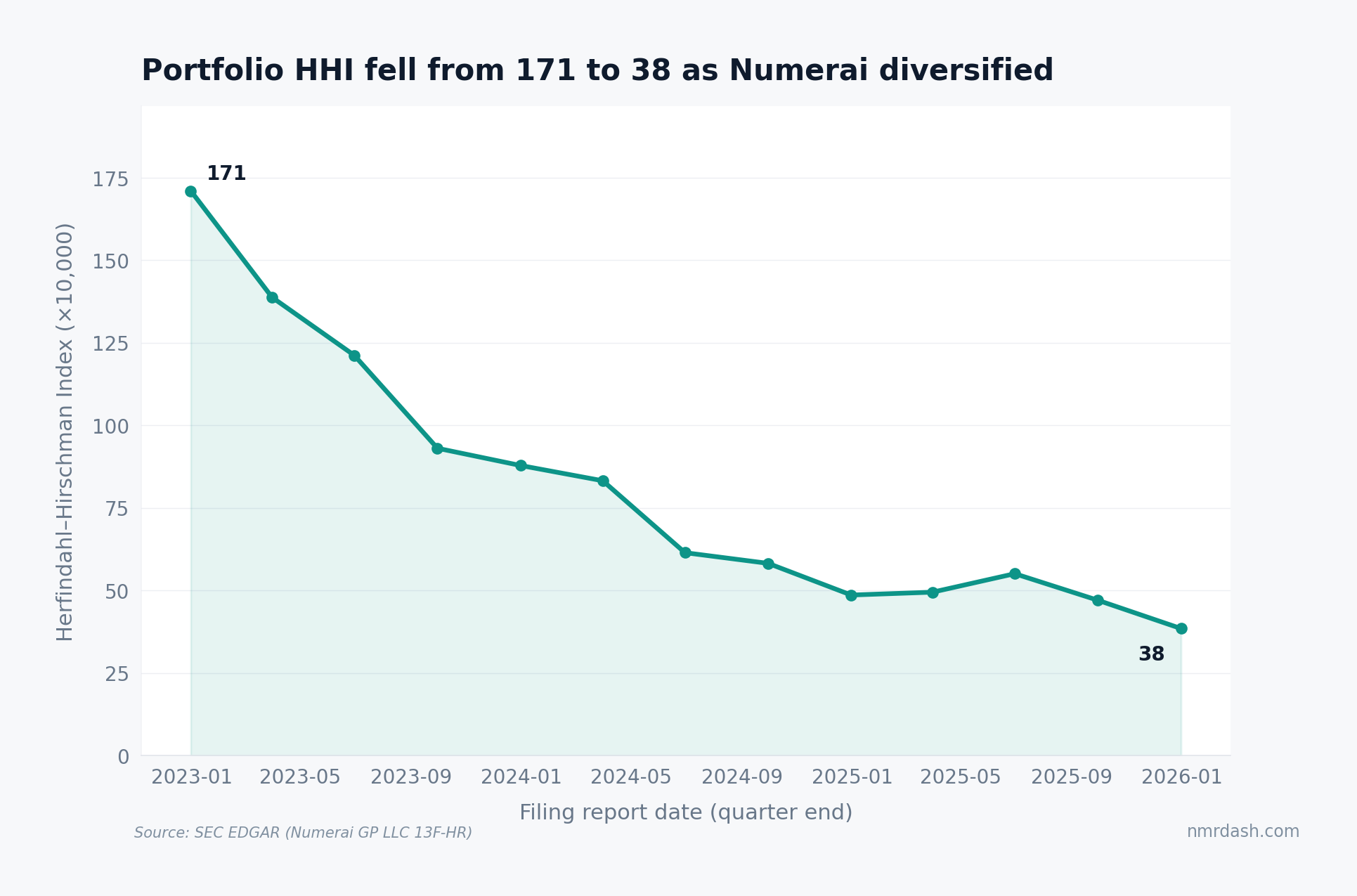

Concentration is unusually low and falling

The Herfindahl-Hirschman Index, defined as the sum of squared portfolio weights scaled by 10,000, fell from 171 in the first filing to 38 by year-end 2025. A single 100% position scores 10,000; an equal-weight 100-stock portfolio scores 100. Numerai's HHI of 38 implies an effective holding count around 260, roughly 43% of the 608 nominal positions — the gap shows the book is long-tailed, not equal-weighted.

Falling HHI is consistent with a systematic equity strategy. A flatter book lowers idiosyncratic risk per position and lets the model express many small bets at once. When the edge is statistical, breadth matters.

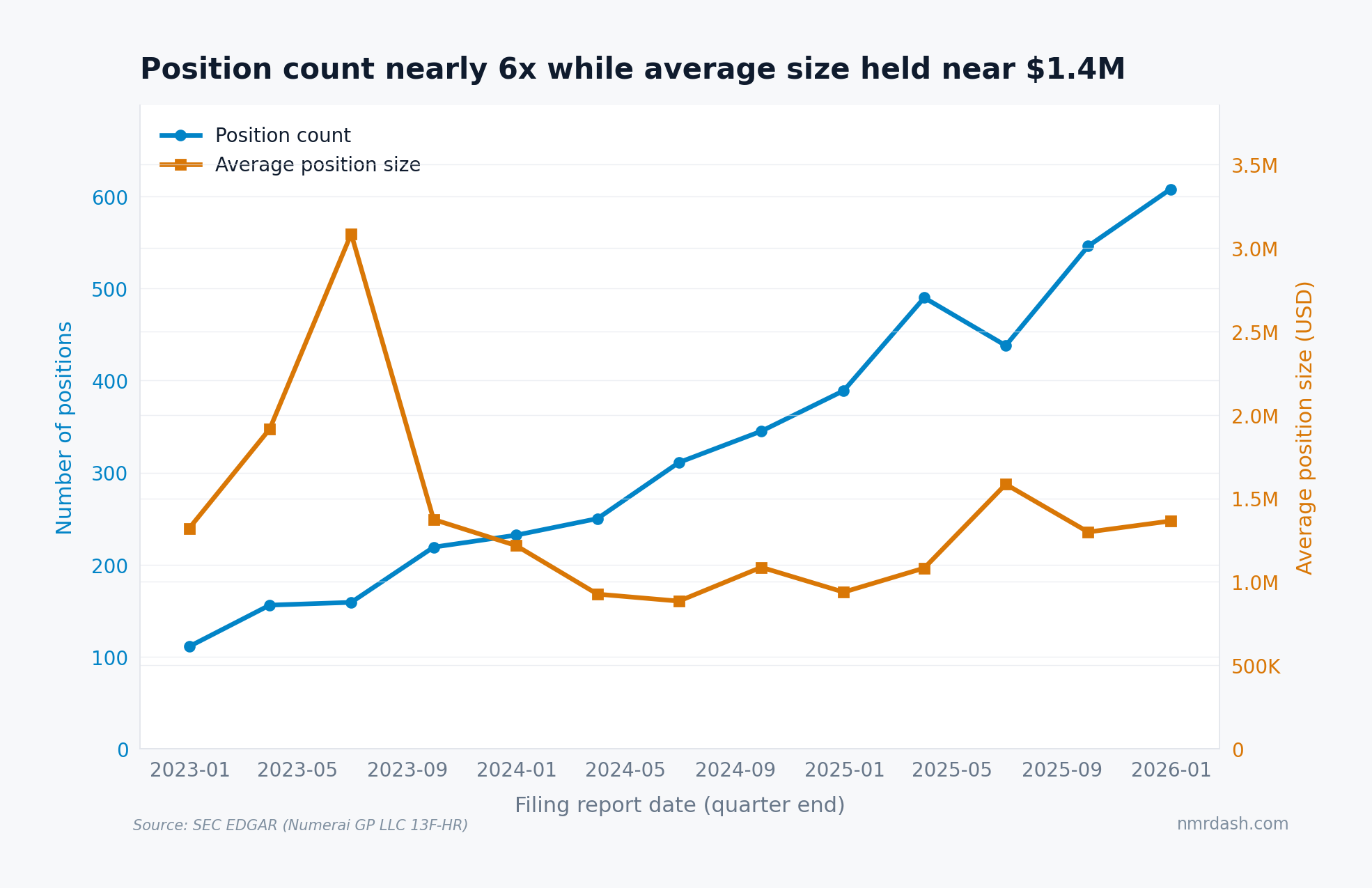

More positions, similar bet size

Position count grew nearly sixfold, from 111 holdings in the first filing to 608 by year-end 2025. Average position size stayed in a tight band around $1.0M to $1.6M for most of the window, with a brief excursion to $3.1M in Q2 2023.

That pattern reads strategy more cleanly than the headline AUM line. New money is deployed mainly by adding names rather than sizing existing positions up. The book is widening, which lines up with falling HHI and with how a model-driven portfolio naturally grows: the cross-sectional signal stays the same, capacity comes from breadth.

Position turnover is also extreme. Of every CUSIP that has appeared in a Numerai 13F, zero show up in all 13 filings. Only 4 CUSIPs persisted through 10 or more quarters — Axon Enterprise and Spotify Technology at 11, then First Financial Bankshares and DoorDash at 10 — while 481 of the 1,541 distinct CUSIPs appeared in just a single filing before rotating out. A typical long-only manager keeps the same dozen anchor positions for years; the model-driven turnover here is closer to a statistical-arbitrage book than a Buffett-style portfolio.

What the book reveals about the strategy

The 13F is the closest public window into how Numerai trades, even though the fund is famously a crowdsourced quant operation built from tournament submissions. The numbers tell a consistent story.

With the largest position at 1.06% of NAV and no holding persisting across the full three-year window, this is a basket strategy where each name is a small expression of a model, not a concentrated thesis fund.

Capacity has scaled by adding breadth, not size. Reported value grew 5.6x against a 5.5x growth in position count, so the firm bought more diversification rather than bigger bets. Average position size barely moved.

Single-name risk is low. An HHI of 38 is far below a 100-stock equal-weight book, though still above the theoretical equal-weight floor for 608 names. The 13F cannot reveal shorts, leverage, factor exposures, or execution risk, so it is only a partial view of the strategy.

For more on Numerai as an institution, see Numerai SEC Filings for the regulatory footprint and NMR Token Economics for the on-chain side. The holdings dashboard refreshes after every new 13F.